By Amit Bakhirta

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning…”

Henry Ford (citing U.S. President Andrew Jackson, 1834)

The 2020 pandemic fuelled a severe economic downfall that led the Bank of Mauritius to engage in a loosening instance wherein the Key Repo Rate (KRR) was slashed to 1.85%, thereby allowing real interest rates to turn negative as headline inflation ended the year well above their initial forecasts at 2.5%. The gross domestic product (GDP), on the other hand, is likely to have dropped by -14% to -15% in 2020. Given 2020’s low base, a mathematical rebound (from that low base) is indeed likely, but the quantum of that rebound may turn out to be weaker than initially forecasted, as Mauritius’ borders remain closed, at least at this stage until March 2021.

Whether it is 6% or 8% of a rebound that Mauritius will experience in 2021, two things are almost certain. Primo, inflationary pressures are likely to be maintained, and secondo with a technical rebound in GDP, the velocity of money (recovering from an unprecedented 10-year slump) is ticking higher. Consequently, the KRR is seeming increasingly hawkish, and this heightens credit risks in the Mauritian economy.

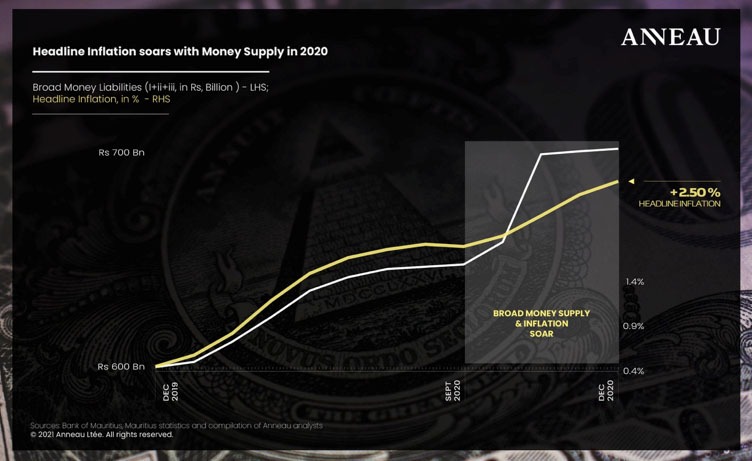

Broad money supply soared and velocity of money dived

Broad money supply, typically consisting of currency held with the public, deposit liabilities (73% rupee deposits and 18% foreign currency deposits) as well as debt securities, grew by an estimated 10-year high of +15.6% in 2020 (almost double its 10-year annual average growth rate of 8%) to an estimated Rs 696 billion in December 2020. As the loose monetary stance worked its way through the transmission mechanisms, the last quarter of 2020 saw the money supply in the Mauritian economy soar, with the month-on-month growth in broad money liabilities increasing by a mind boggling 5.8% in October versus a 10-year monthly average of hardly 0.70%.

On a medium to longer-term perspective, inflation has been empirically found to move in line with broad monetary aggregates. This relationship holds through time, as well as across countries and monetary policy regimes: it is “hardwired” into the deep structure of the global economy. Empirical evidence confirms this relationship, naturally also for Mauritius. This therefore underpins the prominent role which should be assigned to broad money in the Bank of Mauritius’ monetary policy strategy.

The velocity of money is important for measuring the rate at which money in circulation is being used for purchasing goods and services. It is used to help investors gauge the health and vitality of an economy. High money velocity is usually associated with a healthy, expanding economy and vice versa. With the material drop in nominal GDP in 2020 and the increase in the money supply, the velocity slumped to a multi-decade low.

However, the downtrend in Mauritius’ money velocity clearly has been a long-term trend (as evidenced since 2014), which empirically reflects the economic law of the inversely proportional relationship between money supply and the velocity of money. If the money supply in an economy falls short, then the velocity of money will rise (hopefully fuelled by an increase in the number of transactions via higher consumer spending and especially in the Mauritian economy; credit growth), and vice versa.

Money velocity fortunately has turned since September 2020 and we expect this leading indicator trend to be maintained in 2021, as nominal GDP recovers. Whenever the interest rate on financial assets is low, the desire to hold money falls as people try to exchange it for other goods or financial assets. As a result, the velocity of circulation rises.

GDP growth forecasting

Even before the lockdown and pandemic, last year’s 1st quarter nominal GDP had weakened -0.3% to Rs 116.9 billion. Now with the frontiers remaining stubbornly closed and with no tourism receipts and tourism’s negligible contribution to GDP, we do not foresee the 1st quarter GDP exceeding Rs 116.9 billion but rather, in line with the second half of the 2020 trend, we are expecting a slowdown of roughly -10% or more towards the Rs 105.3 billion marker.

Hotels are empty throughout the island. AirBNB starting to feel the dust and hotel and accommodation affiliates are diving and closing after what is looking as a one-year of Black Swan for them! Extending the border closure beyond April 2021 will take Mauritius to more than 1 year of NIL tourists and you can only imagine the catastrophe we are stubbornly heading towards. Already it is unlikely to expect a full reopening before July 2021 (the Wage Assistance Scheme has been extended to June 2021) and so we are likely to miss both the Easter and European Summer vacation seasons, yet again!

By some miracle, if the first quarter GDP exceeds Rs 117 billion, this would have set the tone for a truly strong 2021 recovery; which is highly unlikely at this stage. However, we need to realistically understand that first quarters have and always remain our weakest nominal quarters!

This is where matters get even more interesting. In 2019, our second quarter nominal GDP stood at Rs 124.2 billion. As we confined the entire country in the second quarter of 2020, that GDP had slumped roughly 32.5% to Rs 83.8 billion, resulting in a bankrupt government as fiscal receipts nosedived! Assuming an approximate 25% pick up in these awful numbers takes us to roughly Rs 104.5 billion of nominal GDP in the second quarter of 2021, and this is where we start to get more comfortable and aggressive in our GDP estimates for 2021 (assuming that the vaccines have now reached our shores, our borders wisely reopen, especially to countries with low active cases in a first stage, thereafter by June, to all countries, albeit amidst a strengthening of our tourists momentum and vaccination protocols).

Wealth disparity is widening and real disposable income growth has not been gratifyingly inclusive.

Should the Mauritian economy turn around by June-July, it shall set the tone for an even stronger second half of 2021, and so an estimated average GDP growth of 11.8%, taking us to approximately 8.4% growth in 2021 with nominal GDP ending the year at Rs 464.1 billion, which at this stage, seems a reasonably best case. However, we remain far therefrom as a base case hovers around the 6% marker, which shall likely stiff the needle. As long as the official fourth quarter 2020 nominal GDP numbers are not officially released, estimates for 2021 GDP growth are unlikely to be precise and shall in our humble opinion, require mid-year adjustments.

Growth or Inflation: a central banking headache

As alluded to last year, the Bank of Mauritius has indeed kept its blinkers on inflation. Initially, expecting a moderate headline inflation despite red signs everywhere (as the Mauritian Rupee nosedived), and thereafter simply not attending thereto. The fact of the matter remains that we ended the year with a KRR of 1.85%, a median savings rate of 0.38% and with a headline inflation of 2.5%. Thus our monetary environment is producing negative real rates, which should be ultimately corrected for our nation’s prosperity. Analysing freight inflation, food inflation and medicine inflation, the numbers would be significantly higher.

A peak into our producer price index (for the manufacturing sector), the construction and import price indices, and they are all sitting at a decade high. With nominal GDP growth likely to exceed 6% this year, we now expect the Bank of Mauritius to have enough of a manoeuvre to start tightening its monetary policy instance in order to counter the imploding inflationary pressures (see graph).

A responsive and agile monetary instance by the Bank of Mauritius and its Monetary Policy Committee members is but of essence for a sustainable and durable economic growth of a country. Else, expensive growth (especially when it is highly levered) gets diluted. To understand this concept empirically, Mauritius has grown its nominal GDP by roughly 22% over the last decade, but headline inflation over the same increased by a cumulative 32.2%, and hence adjusted for headline inflation, the economy has shed -10.3% from 2010 to 2020! This remains worrying and this is why the wealth disparity is widening and real disposable income growth has not been gratifyingly inclusive. In simple terms, over the long term, it is essential that the differential between economic growth and inflation widens in a sustainable manner.

Credit risks for highly leveraged companies

In reality, the central bank shall face an enormous pressure to maintain interest rates as low as possible for as long as it takes, in order to stimulate the economy and fuel a recovery (but none the least to help alleviate the executive’s debt servicing pressure of our burgeoning fiscal deficits).

A sustainable credit growth, especially to private households, shall ensure a sustainable turnaround and fuel the turnaround in the velocity of money. We note that as at the end of November 2020, credit growth in our economy has increased by hardly 2.3% to Rs 389.7 billion, against a year-on-year CPI inflation rate of 2.7%. Hence as at November, real credit growth rate was -0.40% in line with the underlying credit deceleration in the economy for the second half of 2020. In the same period, credit growth to the accommodation and food service sectors had increased by a staggering 28% while logically their consolidated revenues must have dropped by almost 75%!

Dealing with an interest rate turnaround in a low growth environment is extremely tricky.

Now this is what we identify as increased systemic risks in the Mauritian economy as these risks towards the meagre revenue and free cash flow generating hotel sector are not being borne entirely by the banks but rather by the nation’s reserves at the Bank of Mauritius and the Mauritius Investment Corporation! This increase in leverage needs to be closely monitored as it affects the value of the rupee directly (it already shed in excess of 18% versus the Euro last year! With our forecast for EUR/USD finding resistance at 1.24 in 2021 and 1.30 in 2022, we cannot but be overly cautious). A number of companies and private households have over levered as interest rates shot lower in 2020 while their incomes weakened.

Now that interest rates are increasingly looking hawkish, in our humble opinion, a number of these borrowers shall face higher borrowing costs and a debt servicing quantum increasing quicker than their net revenues, especially in a subdued growth environment, hence our humble and cautious note. Dealing with an interest rate turnaround in a low growth environment is extremely tricky if the free cash flows of an individual or a highly levered company are not disciplined.

This is the very reason why we expect the Bank of Mauritius to maintain its support to credit growth for an extended period. It shall, at a point of time, have no choice but to start tightening interest rates in the economy to match the higher economic growth but most importantly to counter inflationary pressures which are likely to continue ticking higher, on supply push (plausibly higher than the central bank’s 3% headline inflation estimate for 2021).

The ergodicity problem in economics

The role of global central banking in today’s modern and the future economic world, but most importantly in modern capital markets, is yet to convince everyone. Our issue is that the printing press is being pressed as a panacea every time capital markets stress out ahead of a crisis. This policy, yes, has always helped in all crises (for centuries now), but to until when? Global investors do not fight against a central bank’s policy especially when there is money printing. They follow it. But too much of the print press too quick can ultimately distort risk premia dynamics in the economy; it ultimately eliminates risks, which cannot be engraved and is certainly not natural.

This crisis should be wisely used by our nation’s economic forces as an opportunity to rethink and innovate for the future.

In 2021 this crisis should be wisely used by our nation’s economic forces as an opportunity to rethink and innovate for the future. Time should, in our humble opinion, not be spent on debating the elusive precise estimate of the quantum of our growth this year or the next or thereafter but rather on our desperate need of economic rejuvenation.

As such, to quote Ole Peters, “economics typically deals with systems far from equilibrium, specifically with models of growth. It may therefore come as a surprise to learn that the prevailing formulations of economic theory (expected utility theory and its descendants) make an indiscriminate assumption of ergodicity. This is largely because foundational concepts to do with risk and randomness originated in seventeenth century economics, predating by some 200 years the concept of ergodicity, which arose in nineteenth century physics. In this perspective, I argue that by carefully addressing the question of ergodicity, many puzzles besetting the current economic formalism are resolved in a natural and empirically testable way…”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Stay In Touch