By Sameer Sharma

A term sheet with more details has recently given us a very accurate picture of how the Mauritius Investment Corporation (MIC) is wrongly structuring convertible bonds. Back in March 2020 when Mauritius entered its first lockdown, I extensively wrote and communicated about the need to create a bailout fund which would provide support to systematically important companies operating within at risk sectors. Given that I was one of the main sources of the whole idea in the first place, I cannot claim to be against the philosophy of bailing out firms in specific circumstances during tail risk events, but deals need to be fair.

What was proposed then was that the government should create a Special Purpose Vehicle with at least MUR 5 billion of taxpayer money in the form of equity which would be augmented by leverage tailored on a deal by deal basis in order to create a war chest which would be used to bail out distressed firms that met a certain size criteria. To be more specific, the idea was to create a structure similar to a Protected Cell Company (PCC) where each cell would hold a distressed investment and be financed independently from the other cell.

When it came to debt financing, the Bank of Mauritius (BoM) would purchase bonds issued by the PCC or by each cell (depending on the deal and terms), but such financing would also be open to banks and institutional investors. The Board of this PCC would be made up of investment professionals hired locally and abroad given the lack of local experience in distressed debt investing, and this Board would also be advised by a global advisory firm of repute and experience in distressed investing and pricing. The General Partner would obviously appoint a fund management team which would have previous experience in private equity and hybrids, especially in the domain of special situations and distressed debt.

Unlike what is all too often mentioned in Mauritius, the idea of the MIC was to invest across the capital structure of the firm, and it would also be able to provide liquidity in the form of working capital to companies on a discretionary basis as long as such investments met its long term investment objectives. In sum, the MIC, which would be run independently of government (the government would be passive, and this would be specified legally), could invest in common equity, in preference shares, in hybrid debt such as convertible bonds and in more senior unsecured and senior secured bonds and instruments and finally in other shorter term credit instruments/loans such as working capital loans.

In terms of the MIC’s objective, the idea was for the MIC to be a special situations bailout fund which would aim to better equip systematically important firms with the balance sheet which would allow them not only to face the pandemic but to allow them leg room in order to protect jobs and re-engineer their business models. The MIC would aim to achieve average annual returns in excess of 11% over a 10-year investment horizon, and similar to how things are done within the private equity world, it would seek to exit its investments via various channels during that time period. More importantly, when it came to risk and burden sharing (11% is low for distressed investing), the MIC, when engaging in each deal, would negotiate terms in the public interest given its return objective and would seek burden sharing between majority shareholders of distressed firms and commercial banks which benefit from such bailouts.

Commercial banks are risk-taking institutions when they lend and set capital aside for such reasons, and the MIC would certainly never become the sole Sheriff in town. The MIC would have good governance, it was meant to be accountable to parliament and would publicly release annual fund manager reports, clearly explaining how public money and borrowed money is being invested in distressed assets. The MIC had nothing to do with a Sovereign Wealth Fund. These are different things but got mixed in together in the end.

Conflicts of interest

Contrast what I explained above with what actually happened. The MIC today has a Board with no previous experience in distressed and special situations investing, and nor do any of its staff. Hiring people as intelligent as they may be from different public bodies or with corporate banking backgrounds will not have the same skills set which is required here. When managing special situations fund with leverage on top of it, you actually need people with relevant and previous experience doing the exact same thing. You also need to work with lawyers who have experience in this field and have advised other private equity firms across Africa at least focusing on similar deals. The first rule of good governance to have the right people at the right places is hence broken.

The MIC investment process is quite opaque.

Secondly, beyond a badly designed website which shows little, the MIC investment process is quite opaque, and nor do we know about whether any advisors and law firms that are advising it have any conflicts of interest. Mauritius is a small country with an unsophisticated investor base when it comes to such investment types (never done before here). Because of excess liquidity, one interesting local rating agency and the lack of proper analysis, credit risk has historically been mis-priced. We also know that in a country with few deals from the same small number of corporations, such things can potentially lead to conflicts of interests on the advisor front.

Let us also be honest about our financial sector, it has never done such sophisticated things in the past, certainly no government-owned or state sponsored entity ever has done anything close to this. To make matters worse, the MIC being a curry of a Sovereign Wealth Fund and bailout fund now also invests in infrastructure and other next generation sectors too. Even major alternative fund managers such as Blackstone do not have the same team and Boards managing such diverse investment strategies.

The skills and experience levels required to manage an infrastructure fund versus a fintech fund versus a bailout fund are not the same. These are specialized fields, but somehow the same Board and MIC team with no previous experience in any of these fields can do it all. Either Mauritians are smarter than people who work on Wall Street, or there is a major problem.

Suicidal leverage

What is even more shocking is that the MIC is funded with MUR 1 billion in equity and more than MUR 79 billion in debt. This kind of leverage ratio is outright suicidal, and nor is it tailored to optimize the capital structure of the MIC, and more importantly nor does it tailor leverage on a deal by deal basis within separate cells. While no professional ever leverages structures to this extent, high levels of leverage in such structures need to be compensated for by over-collateralizing massively each deal and by also essentially having a first rank on all assets as well. We need to remember that recovery rates for distressed investments are quite low.

When it comes to public infrastructure projects, you need to have a clear sense of cash flows, and your exit mechanism needs to be well thought through. How investing in drains will meet such criteria are things that are only possible in Mauritius! You are essentially taking on 79:1 leverage to invest in non cash flow generating assets such as drains with no clear exit mechanism over 10 years. The assets themselves cannot be sold to anyone else even if the MIC fails to honour its BoM loans, so the whole structure is a risk management nightmare.

When it comes to its distressed debt sub-portfolio, the MIC seems to, on paper at least, only be investing in “convertible bonds”. Convertible bonds are essentially hybrid securities with equity kickers in the form of a conversion option. In financial engineering terms, a convertible bond of the kind the MIC has been investing into can be priced by breaking down the convertible bond into two main components: a plain vanilla coupon paying bond and the embedded conversion option.

From Black Scholes to the use of multi factor models (including machine learning which is increasingly being used to price fixed income securities), there are many ways to price such securities, but there are some fundamentals which no model can be divorced from either. So, what can impact the price of a convertible bond, and why is this important you may ask? Well, the MIC is an investor taking on a lot of risk given the distressed situation of firms, and the MIC itself is being funded with a 79:1 leverage ratio, so losing a lot of money by for example overpaying for something for 100 when it is worth say less than 70 is a direct mark to market loss from day 1. The value of the option embedded within the soon to be issued New Mauritius Hotels (NMH) convertible matters.

The worst type of deal for a highly levered MIC

One of the first problems with the NMH deal, which shares many similarities to the Lux* deal, is that the conversion price is set very far away from the current stock price when issued. NMH Ltd is currently trading at MUR 4.50 while its conversion price is set at MUR 7.4529, representing more than a 65% premium to the current stock price. I cannot find a single deal over the past 20 years in any global market of repute on a Bloomberg Terminal where a premium has ever been set so high, and mathematically there is a reason for this. It is because the Delta of the convertible bond will equal zero, that is, the sensitivity of the price of the convertible to changes in stock prices is nil. Just with this and accounting for the 9-year lifetime of this convertible, the option value collapses.

The NMH deal is legal but stupid for the MIC and tragic for the public.

You can have 30% to the rare 40% premiums for higher quality investment grade names, but be it high quality or be it for the junkiest of junk rated issuers, you never see such premiums. The premium of 65% of course reduces the conversion ratio which is to the advantage of NMH shareholders versus the MIC.

Then like the LUX* deal, we also have something quite atypical for convertibles, the issuer can call back the bond at any time (with some slight adjustments to notional before and after 4 years), but the highly leveraged MIC investor, who is bearing all the risk in distressed times with a 3rd ranking floating charge, can only convert the bond to equity after 9 years, assuming the firm even survives that long (probability of default is not low for a distressed firm obviously).

Across the globe, the reverse is true. The issuer can call back the bond after 5 years for a 7 or 10 year maturity convertible while the investor can exercise the option at any time whenever the price of the stock of course goes above the conversion price (it would be stupid to convert otherwise). Globally the conversion option is one that is more American in nature while the MIC has gone for a European type option (conversion only at maturity). You do not need to be a structuring guru to realize that American style options (technically it is an American hybrid given soft calls and issuer callable features) have more value than European options because they can be exercised at any time.

Regarding NMH, technically we do not need to talk about other terms in the term sheet because the option value in itself is already zero. We essentially have a 3.5% coupon 3rd rank floating charge subordinated plain vanilla bond with some financial covenants (the only good thing on a poorly written term sheet) which, assuming they at least got the credit spread right, is worth significantly less than the price the MIC will pay for it. The upside returns are capped to a plain vanilla bond with all the risk being borne by the MIC. It is a great deal for NMH shareholders and for the banks too because the latter are able to reduce their credit risk given the bailouts. One bank even paid a dividend recently while public money is being used to bailout firms which banks would have needed to do something about had there been no MIC.

Figure 1: Bloomberg Terminal Snapshot of NMH Deal Replicating Term Sheet

Using the Black Scholes pricer function (other prices will not make a difference given the math of the structure) leads to a cheapness of -47%. The MIC overpaid for the bond by quite the margin.

All the option Greeks are zero and the price of the bond is close to its bond floor, but the MIC will be paying 100 for it. In order not to lose money, it will need to hold the bond until buyback or maturity with capped returns without any conversion value and upside. Shareholders of NMH have zero risk of ever getting diluted, and they should be proud of their negotiators.

We should stop calling this a convertible bond but rather call this a 3.5% coupon subordinated corporate bond with the MIC paying extra money for a worthless option. We can only pray that the company does not default. How will any auditor break down the bond and the option and show the latter having any value will require a new theory in quant finance to be invented.

This is the worst type of deal for a highly levered MIC but fundamentally symbolizes all that is wrong with our system and how deals get made between public entities and the Mauritian private sector. The NMH deal is perfectly legal but also perfectly stupid for the MIC and tragic for the public. Why anyone would structure a deal in such a way is best left to the readers’ imagination.

How should the MIC have structured the deal, you may ask? Beyond keeping some of the financial covenants in the term sheet as is, it should structure the convertible just like it is done by professionals on the rest of the planet. This is not a big ask.

| Coupon (%) | Premium (%) | |||

| 30 | 32 | 35 | ||

| 4.25 | Theo Price | 103.145 | 102.489 | 101.546 |

| Bond Floor | 78.687 | 78.687 | 78.687 | |

| Delta | 56.333 | 56.138 | 55.824 | |

| Implied Vol | 20.377 | 22.422 | 25.29 | |

| 4.5 | Theo Price | 104.161 | 103.521 | 102.6 |

| Bond Floor | 80.345 | 80.345 | 80.345 | |

| Delta | 55.015 | 54.836 | 54.544 | |

| Implied Vol | 17.147 | 19.275 | 22.131 | |

| 4.75 | Theo Price | 105.175 | 104.55 | 103.65 |

| Bond Floor | 82.003 | 82.003 | 82.003 | |

| Delta | 53.702 | 53.537 | 53.268 | |

| Implied Vol | 13.706 | 16.01 | 18.949 |

Figure 2: Proper Structuring of NMH Deal Using Bloomberg Conv Pricer

Essentially, you would need to price the credit risk which, given the fundamentals and Bloomberg derived Distance to Default calculations, should be set at around 400 basis points spread. You would need at least a 4.5% coupon and more importantly you would need: 1) a premium for the conversion price not exceeding 30% on top of current stock price, 2) American style option allowing the MIC to convert at any time, 3) the issuer having the ability to call back the bond any time after 5 years, 4) taking the historical volatility of the stock at 30% (based on current vol), 5) capping some of the upside returns for the MIC with a soft call trigger of 130%.

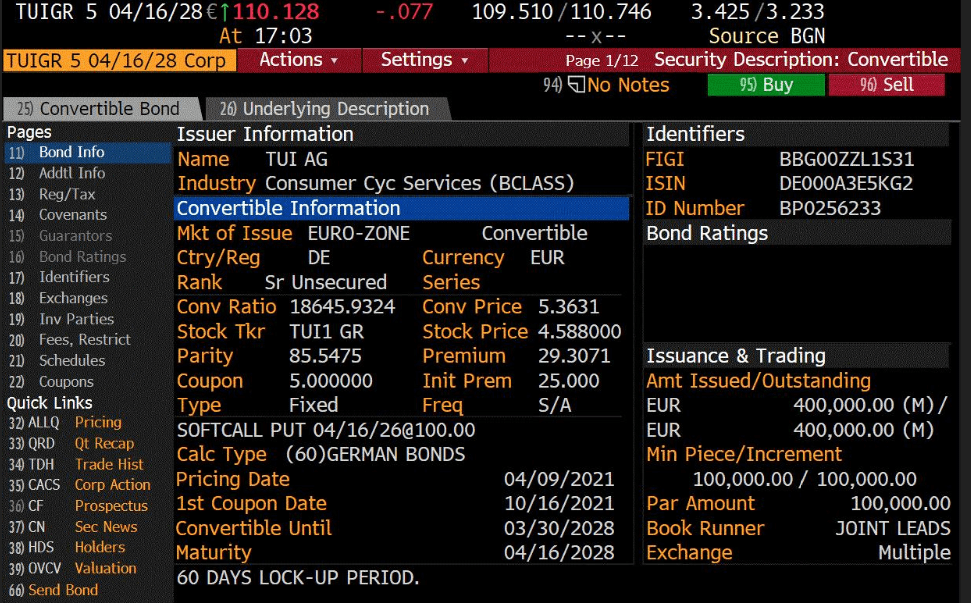

Figure 3: TUIGR Convertible Main Terms

To show how deals get structured outside of Mauritius, here is a recent deal for TUIGR (see Figure 3, note the premium and coupon for example) which is certainly much less one sided than the NMH deal. The Mauritian state must be quite rich for such give aways, but it does not work that way in the rest of the world.

In the case above, pricing of the bond is even cheap as noted in Figure 4.

Figure 4: Pricing for TUIGR is Cheap

Mark to market loss

Under IFRS-9, the MIC will need to mark to market convertible bonds, especially when made to distressed firms. How the auditor will get around the mathematics of how convertible bonds are priced outside of Mauritius will be interesting to watch and one day challenge, but it is clear that the MIC should appoint a credible global advisor to not only explain to its Board that they are mis-pricing convertibles, but also not to make the same expensive mistakes again. We do not turn into bond structuring experts by being nominated to a post and nor do we use public money in such ways.

We may never see a term sheet on the other non-listed deals and other exotic investments such as those to be made in drains, but we are talking about holes and more holes here when it comes to losses. Hold to maturity or hold to call and pray for no default with petty returns for the risk taken is all the MIC can hope for on this deal now. It will technically make a mark to market loss from day 1, which will gradually decline over time. No one in their right mind would ever buy the bond as they would make the loss unless of course they discount it to fair market value. The MIC is stuck with a badly priced bond which is not convertible.

The real mark to market loss from day 1 will be significant in reality, no matter how one attempts to account for it. Such deal making skills does not speak volumes about Mauritius’ global financial centre. Of course, the MIC could have gone for a simpler structure like a preference share or even discounted land value for cash deal, but they went for something which some may think is like a bank loan without understanding the mathematics behind option pricing. It is high time for the whole MIC structure to be revamped.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Stay In Touch