By Sameer Sharma

The restart of economic activity globally has broadened and is still running moderately ahead of expectations in developed markets. This is reflected in trends seen in high frequency economic and alternative data which pushed the likes of the International Monetary Fund (IMF) to upgrade the near term global growth outlook for developed economies in particular in recent weeks. While covid-19 infection rates remain high in the United States and are picking up once again in Europe, fatalities as a percentage of total cases have fallen, and hospitalization rates have only risen moderately. With our ability to manage death rates and severe cases improving, there is a data driven realisation that economies need to be opened for business in order to manage the risk of a potential social crisis and of rising credit defaults. Shutting parts of an economy for long periods destroys corporate balance sheets with longer term consequences on private investment and unemployment. With government debt globally now quite high, there is a realisation that there would be little leg room for continued fiscal stimulus to pick up the slack of a more zombie like private sector.

The pandemic has also taken the world closer to full blown Modern Monetary Theory territory than MMT theorists could have ever imagined. This blurring of monetary and fiscal policy essentially means that having proper checks and balances on fiscal policy makers accessing the printing press becomes all the more important. In the absence of such guardrails, there is a real risk, especially in the case of Mauritius, that the central bank could lose grip on inflation and inflation expectations. This is particularly concerning for a country whose monetary policy makers have consistently failed to define a quantifiable flexible inflation target. Transmission mechanisms seldom work well without properly anchored inflation targets and a framework around them. However, over the past 7 years, global inflation has remained low, and until the crisis, large foreign exchange flows into Mauritius had kept the nominal effective exchange rate of the rupee from depreciating, allowing for low and stable prices locally. Luck is about to run out in the coming years especially post 2022.

Ill-designed and issuer-biased large corporate bailouts

Mauritius has gone further than almost any other country on earth in terms of central bank financing as a percentage of its GDP in recent months when it comes to both helicopter money grants (even a simple understanding of central bank balance sheets and asset liability matching would invariably lead to helicopter money financing of the grant) and foreign exchange reserve sales in order to fund ill-designed and issuer-biased large corporate bailouts, but with very little to show for it so far given how many of the schemes have been designed and implemented so far. As a good friend of mine likes to say, you have to come to Mauritius to hear things like a convertible bond with near zero delta and hard call provision (barely any equity sensitivity given how they are being structured) having magical convexity coming from the option component and becoming like “quasi equity”.

New theories of quantitative finance aside, while supporting systematically important companies is important and arguably necessary and was pushed forward by this very author back in February, this is public money. When a central bank builds international reserves, it pays for it in the form of monetary policy instruments which cost it dearly. International reserves are also our insurance policy against global collapse, so the sacrifices need to be shared by everyone, be it banks, the public and the companies themselves. While the funding of the Mauritius Investment Corporation (MIC) should not have come from foreign reserves but from debt purchases issued by an off balance sheet Special Purpose Vehicle in the first place, the MIC should be compensated for the risk it is taking.

Beyond structuring balanced and fairer deals, private equity and special situations investing is about properly sizing the deals, about looking at a broader longer term picture of the industry, about restructuring and industry consolidation and about adapting to new post-Covid realities. These are complex deals requiring experience and skill. With technocracy almost as dead as the Dodo within Mauritian policy making circles, execution and project management of the stimulus become quite the challenge. Grand ideas remain “grand” on paper.

When central bank and fiscal policy coordination without guardrails are combined with longer term structural and secular economic trends such as de-globalization, the related balkanization of global supply chains, rising inequality, associated populism 2.0 and the increased pressure to come on offshore “tax havens” from Western, Indian and African tax authorities in a high debt world, a more stagflationary regime will become a bigger risk for the entire world and more importantly a base case for Mauritius in the medium term. Policy makers must get their act together and soon.

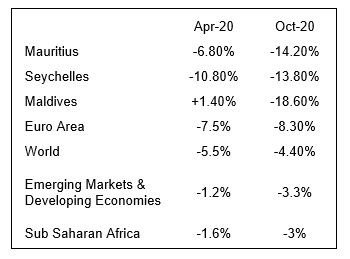

2020 Projection of IMF World Economic Outlook

Policies that need to be implemented

With more than 85% of its GDP in gross public debt and rising, the Mauritian government will need to engage in meaningful structural reforms of the economy. These reforms should include the following.

Mauritius should create an independent Budget Office accountable to parliament.

- Once the global pandemic is under control, the government will need to show a realistic plan in terms of how it will get public debt and unfunded liabilities under control in order to avoid a credit downgrade which will impact local banks which are rated lower or unrated. The least painful tax would be to start taxing the rentier economy via well targeted land value taxation and property taxes. It is high time that some “villages” like Tamarin, Triolet, Grand Baie get converted into towns and be subject to municipal taxes. This is not about vote bank politics but about economic realities and being fair.

- Mauritius should create an independent Budget Office accountable to parliament which will paint a true longer term picture of macroeconomic policy proposals without any spin and Excel sheet (1+r) magic during outer years. It is high time to put some discipline and math behind electoral promises of all parties.

- Significant cost controls of public sector salaries starting with 30% to 50% cuts to base salaries and entertainment allowances of politicians. Similar to Singapore, salaries of nominees, politicians and senior public officials should be based on a combination of a low base salary and performance based bonuses linked to clearly defined long term Key Performance Indicators. Base salaries can be capped while bonuses can be uncapped. For all politicians and government employees, international travelling and perdiems should be paid for via corporate credit cards. There is no need to be driving Series 5 BMWs and the like anymore. Japanese cars will do.

- In the short term, the Bank of Mauritius will need to work with banks when it comes to a restructuring of debt of viable small and medium enterprises. Various options exist from pooling and securitization of central bank guaranteed restructured loans to working capital loans at concessional rates (central bank support) equivalent to 5 years worth of corporate taxes paid. Rules based and transparent approaches to determining whether firms are viable and eligible should be discussed, debated and implemented.

- Seychelles seems to be well ahead of Mauritius at least when it comes to its border re-opening strategy. Mauritius must lead, not copy or follow.

- Listing of 25% to 30% of all government majority owned entities on the Stock Exchange of Mauritius in order to raise much needed funds to pay down debt.

- Shift government savings from cost control measures to help as many of the poor and unemployed as possible. Politicians should live humbly during these times.

- The Mauritian capital markets are stuck in the past because the right people were never put at the right places. One of the reasons why Mauritius should go on a massive re-branding strategy post black list is to promote its capital markets too. Mauritius needs to issue Eurobonds to also gain visibility internationally beyond the back office tag. Eventually Mauritius should have Credit Default Swaps trading on its name and it should ensure that it remains a recipient of cheap dollars from abroad. So it can redeploy this towards dollar starved Africa be it via trade finance, short term dollar reverse repos and swaps or longer term less liquid investments (small portion of portfolio and subject to liquidity management requirements). Mauritius should also put money towards the creation of a proper African clearing house where African and local banks can better manage counter-party risk. It is high time to have a less fragmented local bond market via the complete revamp of the way debt is issued and managed, the promotion of ESG criteria by a less passive public pension fund industry (less passive shareholders demanding better) on listed companies. Is it not high time we catch up to the rest of Africa, let alone other emerging markets when it comes to proper quarterly corporate disclosures (versus abridged accounting which favour as usual the listed companies more than the investors)?

- Redefining and revamping the MIC into a proper sovereign wealth fund manned by accountable professionals along with an enhanced governance framework. This is also true for public pension fund money management where the latter is still stuck in the 1990s in terms of sophistication.

- Strengthening the independence of the Bank of Mauritius with longer 6 year minimum terms and stricter screening for Governors and Deputy Governors. Foreign expert panels from the IMF and the Bank of International Settlement should help advise on hires. Deputy Governors should also be formally accountable to the Governor. Relevant qualifications should be a requirement for all appointments including for the Monetary Policy Committee and the Board. All jobs should be opened to international applications too given the scarcity of skills in Mauritius. The central bank should also be given a clearer mandate in the form of a quantifiable albeit flexible inflation target and be made accountable for it. Unconventional policies should be subject to achieving price stability over the medium term.

- All government run entities and government majority owned companies and institutions need to publish annual reports, need to be provided with clear KPIs and have a similar mix of base salary and performance based bonus. Take State Bank of Mauritius (SBM) for example, the Board and all senior staff should have a much lower base salary and have a performance based bonus paid in cash and SBM stock with clawback provision. The higher the respectability, the higher the share of SBM stock as a percentage of total compensation.

- Developing a new framework for public private partnerships and modernising the asset and pension management industry especially when it comes to having a more modern asset allocation framework which includes alternative asset classes such as infrastructure, venture capital funding and local private equity investing. In order to further democratise the economy, the Competition Commission of Mauritius needs to be revamped.

- Religious bodies, associations and cooperatives have idle cash sitting earning nothing in a decade of higher inflation to come. It is high time to connect the pipes, implement endowment style management of funds and invest in an economy where the government itself will have limits. The over-reliance on traditional bank financing is not good enough. Mauritius must develop a venture capital, private equity and private credit markets. These are the pipes for alternative forms of financing. One interesting symbol of how backward our capital markets are is the mention in the 2020-2021 national budget that a venture capital ecosystem would be created via the Stock Exchange of Mauritius. I have never heard of venture capital and stock exchanges before. We should refrain from being overly innovative sometimes.

Central bank money printing is not a sign of economic strength.

- The immediate hiring of the best and brightest the country has to offer locally and internationally and inserting them into key industries and sectors on the policy making side. The disdain for technocrats must end if Mauritius is to move forward. Renewable energy and the blue economy can create jobs. The plans have existed for years, but the current system does not allow for competence and plans remain on paper.

- Immediately attract the silver generation to Mauritius, the Covid-19 free island. Beyond the silver generation, put the right people at the right places and let them implement the right policies in order to attract a new generation of foreign entrepreneurs and start-ups to the country. Mauritius needs to grow in terms of population.

- The government needs to go completely digital and provide contracts to locals and foreign investors willing to set up shop in Mauritius. The primary focus would initially be to build the data architecture from which data analytics could eventually be leveraged. This would not only bring operational efficiencies but better policy making. Beyond the setup of the data architecture, Mauritius needs to catch up to the rest of the world when it comes to Internet of Things and 5G. Smart cities do not look too smart right now.

- Give more independence to municipalities and district councils to impose the above mentioned land value and property taxes and post capacity building, allow them to raise income via municipal and district bonds. Raised funds could then be used to stimulate the economies of local communities. For example local small and medium enterprises could obtain more public contracts.

- Mauritius needs a more fluid labour force, its education system needs to be completely revamped with a greater focus on quality, and accountabilities need to be clear. Free universities when the level is not good is also worth as much as the degree. For primary and secondary schools, give local communities more power in terms of imposing these accountabilities on school officials.

- Fighting growing wealth inequality should start with political reform towards a more secular and just Republic where the focus should be on equal opportunity which primarily starts with a fairer but high quality education system for all, not just the elite who can afford private schools and multiple tuitions.

- Bailouts must strike the right balance beyond getting a fair share for the risk that is taken in terms of also pushing companies to open up their capital structures to a less passive shareholder base. It is for markets to punish those which do not perform, but when your market itself is flawed, how will you enhance productivity in the private sector too?

- I have only scratched the surface of policies which can and need to be implemented assuming there is a change in mindset at the top levels of policy making before it is too late. Let me be very clear, the economic data has yet to turn for Mauritius especially when we adjust for base effects.Loyalty to the party as the sole condition for hiring and nominations sounds nice in normal times, but in this new world you need competence, or else this country will be doomed and much sooner than we think. After all we need to admit to ourselves that we are already in central bank money printing mode. This is not a sign of economic strength but of something much less sanguine. We were already doing it with the MUR 18 billion Special Reserve Fund transfer pre-Covid-19!

The longer we wait, the more self defeating our next move shall be. One indeed hopes that the leaders of the day can avoid a Zugzwang which means sticking to business as usual and making a self defeating move for themselves and for the country.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Stay In Touch