By Sushil Khushiram

The response of the Bank of Mauritius (BoM) to the Covid-19 shock was initially in line with the monetary policy stance of most other central banks. Interest rates were significantly reduced worldwide, almost touching the lower zero bound in a number of advanced countries. Unconventional quantitative easing policies have also been adopted through heavy bond buying by central banks, to boost liquidity and lower interest rates.

To cope with the adverse economic impact of Covid-19, BoM eased interest rates to 1.85%, and enhanced liquidity conditions notably by reducing the statutory cash ratio of banks to 8%, as well as through other measures, including credit lines to affected businesses through banks and other financial institutions.

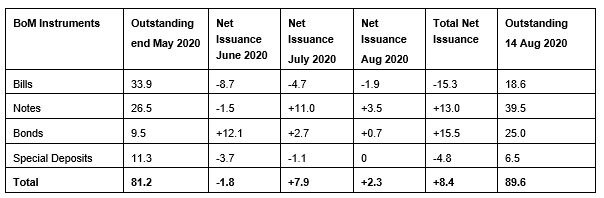

BoM also allowed bank liquidity to rise by letting its monetary policy instruments, comprising BoM bills, notes, and bonds, to mature without any fresh issuance. From a peak of Rs 128 billion at end January 2020, the outstanding value of BoM liabilities on account of its open market operations declined by more than Rs 45 billion to Rs 81 billion at May 2020, mainly owing to the maturing of BoM bills and no new issuance.

Following the announcement of BoM grant financing of the 2020/21 budget by Rs 60 billion, BoM then reversed course on the claim that it intended to raise this amount from the domestic market. BoM thus started issuing BoM bonds and notes as from June 2020. Between end May and 14 Aug 2020, BoM raised a gross amount of Rs 28.5 billion, but maturing BoM instruments amounted to Rs 20.1 billion. Hence, only a net amount of about Rs 8 billion was raised over this period, as shown in the table below.

Bank of Mauritius Open Market Operations (Rs billion)

The reason for this U turn in BoM monetary policy operations is the BoM claim to assume Government’s role in raising budgetary finance. The Governor of the Bank of Mauritius, Harvesh Seegolam, announced on 29 May 2020 that the Bank would issue its own instruments to finance a contribution of Rs 60 billion to Government, and to absorb the ample liquidity available on the market, as a monetary operation meant to promote orderly conditions on the money market. This twin objective to act both as Government’s fund raiser and to conduct independent monetary policy is fraught with contradiction.

To recall, the contribution to Government by BoM is governed by the recently amended BoM Act, at Sec 6(1)(oa), which reads “The Bank may on account of the Covid-19 virus having a negative impact on the economy of Mauritius, grant such amount to Government as the Board may approve to assist it in its fiscal measures to stabilise the economy of Mauritius”. The latest BOM Statistical Bulletin confirms that the one-off contribution of Rs 60 billion to Government would be raised from the domestic market. If the Bank is raising money to finance Government, then it is clearly for fiscal purposes.

Fiscal dominance of monetary policy is now evident.

On the other hand, the issue of instruments for monetary policy purposes is governed by section 6(2)(a) of the BoM Act, namely, that “The Bank may raise, for monetary policy purposes, loans by the issue of Bank of Mauritius securities”. Invoking both fiscal and monetary policy reasons for issuing central bank debt expresses a discordant and muddled view of central bank governance.

Whereas the BoM has been enhancing liquidity since March to stabilize the economy, the intended raising of loans of Rs 60 billion by BoM to reduce liquidity will go against the monetary policy objective to buttress liquidity and ease interest rates. The Bank is trying to raise loans to support fiscal policy, not to meet monetary policy objectives. This is why the public and investors are concerned that the independence of the central bank has been compromised, and that fiscal dominance of monetary policy is now evident.

The contradiction in BoM’s fiscal financing, disguised as a monetary policy operation allegedly to mop up liquidity for stabilization purposes, is apparent. In raising funds for Government, BoM is putting upward pressure on interest rates, whereas BoM monetary policy is seeking to keep interest rates low.

Several auctions of BoM instruments have remained under-allocated, as banks bid mostly at higher yields whereas BoM only wants to issue debt at lower yields. The attempt to mobilize funds from the wider public as from end March 2020 through a 2-year BoM Savings Bond 2020 offering 2.5% per annum, has also shown dismal results, with only around Rs 1 billion raised so far out of a planned issue of Rs 5 billion. Clearly, banks and the public will only lend funds to BoM at higher bond yields, probably because of rising inflationary expectations.

BoM is struggling to issue debt at longer maturities despite the prevailing situation of excess bank liquidity engineered by BoM. Excess cash holdings of banks stood at Rs 39 billion in early July 2020, compared to Rs 16 billion in mid-March 2020. Bank deposits held with the BoM at end July 2020 were higher by about 50%, or Rs 44 billion, than at end July 2019. In June 2020, Government raised a net amount of about Rs 20 billion from the domestic market through its debt instruments, including bills, notes, bonds, and Treasury Certificates, but has since mostly refrained from tapping the market.

Moreover, the auctions of BoM securities are mostly conducted in a two-stage process, which does not reflect a proper and transparent allocation, giving rise to suspicions of manipulation. Funds of state-owned insurance companies and other entities are probably being directed to subscribe to BoM debt instruments at lower yields.

A financial oil spill disaster?

The BoM’s arduous attempt at debt issuance for Government is sowing confusion about the role of monetary policy, and should be terminated. Government should finance its budgetary needs directly from the market instead, without the BoM seeking to position itself as the intermediary. Government’s reliance on the BoM’s contribution for deficit financing will only activate the BoM’s money printing machine and inevitably aggravate the adverse consequences for the rupee and inflation.

Government should finance its budgetary needs directly from the market.

Domestic inflation remains subdued at present, chiefly on account of reduced demand for locally-grown foodstuffs from hotels and restaurants, of existing surplus stocks of goods, and of weak global oil prices. It would be foolhardy to assume that these favourable circumstances will persist, especially for imports in the wake of a rupee depreciation of over 10% during the financial year 2020/21, as well as more difficult trading conditions arising from a disruption in global supply chains.

The need to manage liquidity to fight inflation will unavoidably require the central bank to load itself with further debt liabilities, along with the associated costs. At some point, the only option left will be to inflate public and central bank debt away, mainly through sizeable depreciation. With a prolonged Covid-19 pandemic, the continued transfer to Government of BoM foreign exchange valuation gains arising from rupee depreciation, coupled with more BoM money creation, will inexorably lead to a severe financial crisis.

Proponents of easy money or ‘modern monetary theory’ often fail to make the distinction between advanced economies with strong reserve currencies, and less developed and more open economies where the exchange rate succumbs more readily to expansionary policies and ignites inflationary pressures. Even for advanced countries, the current weakness in the US Dollar and the sharp rally in gold prices calls for caution in handling inflationary expectations.

In the words of Raghuram Rajan, former Chief Economist of the International Monetary Fund, there are limits to public debt monetization by the central bank. This process can go on for a limited period of time, but ends when people start to fear the extent of monetization, being to worry about inflation, and whether the accumulated debt will be paid back or inflated away. Also a former Governor of the Reserve Bank of India (RBI), he recently emphasized the need for the RBI to retain its inflation focus to ensure confidence in the rupee.

There is yet time for the BoM to restore its independence and the credibility of its monetary policy mandate. South Africa’s central bank Governor has so far resisted pressures to ease Government finances, insisting that he is not about to join “central bankers who are pliable” and “overlook their responsibilities”.

Mauritius ended up on an EU money laundering blacklist because of a mistaken adherence to the letter of the law instead of demonstrating an effective implementation of anti-money laundering legislation. We are in danger of a similar miscalculation to join a central bank governance blacklist. Is there reason to hope that a financial oil spill disaster can still be averted despite the rising risks?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Stay In Touch