By Amit Bakhirta

“The inherent vice of Capitalism is the unequal sharing of blessings. The inherent virtue of Socialism is the equal sharing of Miseries…”

Winston Churchill

A budget is merely a consolidation of the means to achieve a nation’s vision, or rather an executive’s vision for the country. It sets public policies as a means towards achieving that very vision. It ultimately aims to further support an inclusive and fair socio-economic development plan. Going past this budgetary exercise is the actual economy, largely founded on an undeniable requisite of a buoyantly ‘avant-gardist’ private sector. We shall rather succinctly herein delve into the limitations of the construction sector’s (especially residential) contribution to overall GDP growth, emphasize the importance of a disciplined balance sheet expansion for the government and reiterate the so under-mediatised but crucial role of the Mauritian private sector in an economic recovery cycle.

An over reliance on construction brings little to economic recovery

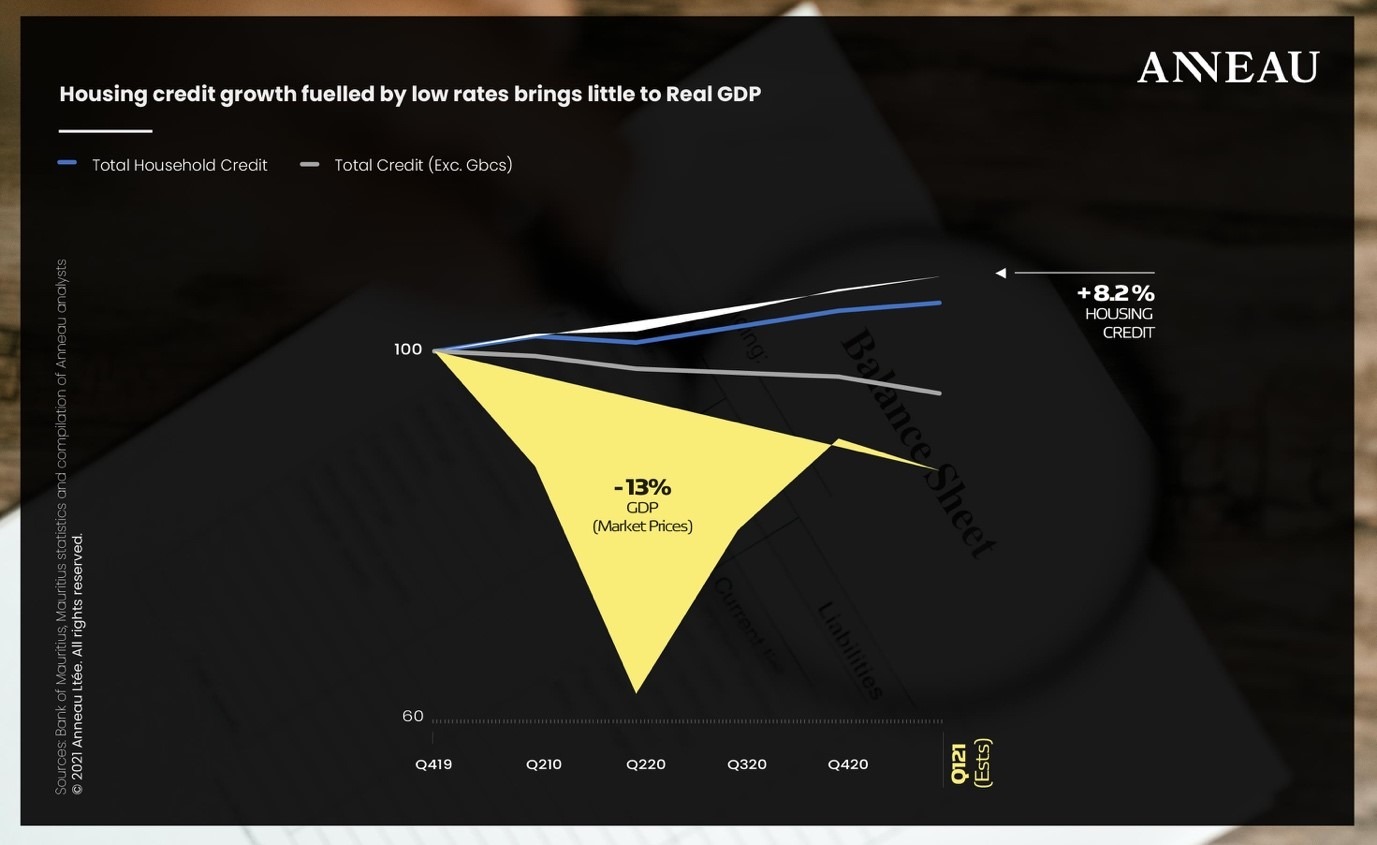

“When construction is booming, the economy is booming…” The tagline can impress the layman but in a real economy, the numbers actually do the talking. Our chart herein clearly demonstrates the actual credit growth in our economy versus nominal GDP contraction, since the last quarter of 2019.

Readers can clearly see a nominal GDP plunging by 15% while overall credit allocation to residential housing (as tracked by the household housing credit numbers) has shot up by roughly 8.2%, as opposed to total household credit increasing by 5.3% and total credit (including the private sector credit but excluding Global Business Companies) slumping by 4.5%.

Yes, as interest rates dropped to record levels (the savings as well as borrowing rates), individuals have been piling up (supported by commercial bankers, of course) on mortgages fuelling this support. One needs to analyse and extrapolate the depicted trend (from last quarter 2019 to March 2021 estimates) before the more inciting budgetary support announcements to the residential property market. Hence, the announced measures are more than likely to fuel this residential credit growth further into 2021-2022. Unless our reading is different!

This progressive move by the government towards more inclusive home ownership needs to be rightly applauded – and adds fuel to a fire already lit, right? Given the fact that the institution has been unable to furnish the promised 12,000 low-cost housing units, and an over reliance on residential construction, this move should compensate.

Weak credit growth

For commercial banks, obviously this is a double-sided move as it helps to eliminate the default risk (being guaranteed by the Bank of Mauritius/Government) but should also technically lead of a decrease in the effective mortgage rate (as the default risks should be almost zero). Mortgage pricing cannot remain the same. The central bank should intervene to ensure the effectiveness thereof. You cannot eliminate risk from an asset class, and the risk premia remains unaltered!

So, the commercial banks’ net interest margin typically generated on residential mortgages (typically tight anyway) are likely to tighten. For the buyer(s), this is heaven and may also lead to risk taking, speculative buying with second or third property purchases for those who can afford – both locals and foreigners. The banks should assess mortgage credit more prudently and responsibly, especially when it comes to speculative buying.

The banks should assess mortgage credit more prudently and responsibly.

Net off, I applaud the move (especially for the low-income earners and first-time young couple buyers). Economically however, it is unlikely to have a major impact on mortgage credit growth, given the fact that almost 85% of the population are already owners of their first property and that the growth has been reasonably well entrenched.

Our argument here is that these measures, as has been the empirical case until now (see chart herein), bring very little net nominal and incremental value to overall GDP growth. On the other hand, it is very likely to fuel a burgeoning bubble over the long term, especially considering that it is has been empirically stated that 85% of Mauritians are owners of a first property, and so the housing deficit in Mauritius remains one of the lowest in Africa (let the 2008 US residential housing crisis serve us an invaluable lesson). This segment, as such, is unlikely to fuel a strong economic recovery.

Overall credit to the general economy has been weak. This is where accommodative policy measures serve to reignite investor and private sector confidence. Overall credit growth in the economy has weakened cumulatively by roughly 4.5% since the last quarter of 2019. The pandemic and the public policy responses, strategies and ‘bail-out’ measures remain obvious culprit(s) – or benefactor(s).

It is natural for bankers to shift their asset liability matching exercise more towards the household sector (they borrow short and lend long), albeit as usual, selectively, in times of economic and financial stress for the private sector. Especially in a pandemic led recessionary cycle, which is particular, to say the least. The numbers talk that overall credit allocation tanked a third the contraction of GDP. And this very credit allocation is key to maintaining the effectiveness of the monetary transmission mechanisms in the Mauritian economy.

Credit extension to the overall private sector needs to be healthy, prudent but also boosted right now. This shall likely extend the multiplier effect on the overall economy. A rapid and smooth deployment thereof supports the velocity of money in the economy, which in certain economic cycles is all thereabout.

The private sector is the real economic machine

Budgets in Mauritius tend to be an event. Wherein 99% of our people’s main question revolves around: “What’s in for me?”. This needs to evolve. Another 1% of thinkers tend to have a better understanding and so delve deeper therein as to the essence, intelligence, tact and underlying impact thereof on the actual real economy, on public finances, on our drowning currency and eventually on our nation’s competitiveness and standard of living over the short to medium term.

The executive should focus on smarter ways to increase revenues through structural reforms.

Does our private sector need continuity in the midst of an ever increasingly complex recession and globalised economy, or does it need rupture? Many times, an arguably sour pill is what is actually needed for higher sustained and much more inclusive growth.

What is the private sector’s proposed ‘budget’, founded on their recovery plans? This is what needs to be analysed and ascertained (at a granular level). The proposed budgetary measures remain merely a framework for the private sector to assess the future with a certain visibility and confidence. This is the economic force which is likely to invest productively (hopefully for some, not for all, as we have empirically noted over the past decades) and so lead a strong recovery. The private sector remains the crucial link in economic recovery.

Stability rarely equates to strong growth

Zones of comfort do offer stability and continuity, but also, if one is not mindful, economic lethargy! It is therefore increasingly necessary to contextualize and also accentuate the importance and the shared responsibility of the private sector (and the credit support thereto) in an economic recovery. Despite a context where the economy is in a recessionary cycle, the 2021-2022 budget offers a certain continuity but also a record over-indebtedness (there’s always a price) wherein in our humble opinion, it is rather the private sector which should be overleveraging its capital structure in this record low interest rates environment and invest productively in the economy, supporting employment and inclusive wealth creation – and so private domestic consumption.

The executive should now be focusing on increased budgetary revenues and a fiscal consolidation plan. The government should hereon be focused on generating higher recurring income to avoid a socio-economic crisis in the longer term. Undisciplined fiscal spending is expensive if unsustainable but can prove to be highly contributory if productive and intelligent.

The executive should therefore focus on smarter ways to increase revenues through structural reforms while balancing social costs. It could consider privatizing certain public bodies of a non-strategic nature coupled with a more progressive and philanthropic fiscal policy over the medium to long term.

It cannot solely be the onus of a nation to over-contribute towards bailing out our government, systemically important institutions and towards socio-economic development. The more fortunate ones should do it as well, in an openly societal and philanthropic modus.

Eventually, the incremental increase in recurring revenues should naturally imply a smarter reallocation of the country’s meagre resources. Fiscal policies, through better management of public finances, help improve the standard of living of the people, not the other way around.

In conclusion, a budgetary process is a movement of public policy. The real economic machine, let us not forget, rightly so, in any economic and political system, remains the private sector. More than ever, the private sector must be the engine of a strong, inclusive and sustainable economic recovery. This revival is not entirely and solely the responsibility of those elected to govern altruistically!

The current crisis offers us an invaluable opportunity for self-assessment, innovation and disruption. And therefore, each private sector participant (large or small) must be able to optimize the budgetary measures proposed to stimulate this much needed economic recovery in an environment founded on capitalist ideologies, supported by responsible socio-economic budgetary policies.

“If you can’t fly, then run,

If you can’t run, then walk,

If you can’t walk, then crawl,

But whatever you do,

You have to keep moving forward…”

Martin Luther King

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Stay In Touch