Par Sameer Sharma

Higher than expected inflation numbers, when coupled with the relative strength of the economy of the United States, kept the US dollar on a strong footing so far this year relative to most global currencies and to the Mauritian Rupee which hit an all-time low versus the greenback and gold earlier recently. While external factors, which include geopolitical risks, have contributed to the Rupee’s continued slide, these exogenous factors do not tell the full story. At the core of the Mauritian Rupee’s ills remains an obsession with a debt-fuelled consumption model in a country in which the bulk of consumption largely depends on imports.

This model in recent years has been accentuated further by the use of central bank money printing to finance badly structured one-sided private sector bailouts and transfers to the government. Money printing, when coupled with continued government borrowing, has allowed the fiscal side to transfer cash to eager-to- spend citizens which in turn has continued to put pressure on the current account deficit, balance of payments and thus, the Rupee. Any current account deficit that is above 4% of GDP in Mauritius tends to lead to a weaker Rupee, and while the pandemic made matters worse, a doubling down on the debt-fuelled consumption model has kept the current account deficit too high.

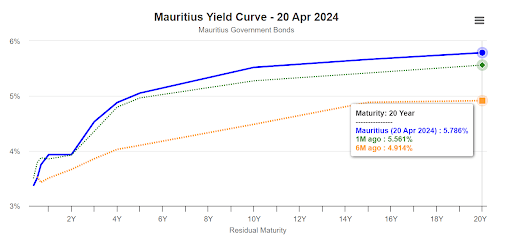

Real interest rates have remained largely negative

Fiscal dominance over monetary policy has meant that both short term and longer term nominal interest rates (bond yields) have remained below both year-on-year inflation and 5-year ahead inflation expectations (5.5%-6% as per various Bank of Mauritius’ surveys). Negative real interest rates have in turn pushed those with savings and forex revenues to seek higher yielding or higher return alternatives, be it in real estate locally or in international asset classes. It should be noted that US short term 3-month treasuries currently yield 5.4% while the Mauritian 3-month Treasury Bill rate yields a mere 3.65% which is not only below local inflation but well below higher quality US paper. Both global and emerging market equity returns ex China have also been far higher than those of local equities over the past 10 years.

Unless the differential between local and international rates falls and unless more return opportunities are generated locally, this trend will continue. Many conglomerates are currently parking their foreign currency earnings in short term US and EU treasuries, which has been a profitable move for them given the direction of the Rupee. Unless the government changes the macro model over the medium term and in the short term imposes windfall profit taxes linked to the Rupee’s depreciation (depreciation boost to revenues), this trend of holding onto forex will continue.

The central bank’s weak balance sheet has affected its credibility

The Bank of Mauritius is supposed to have a medium term inflation target of 3.5%, but since launching its new framework a year and a half ago, it has failed to achieve this goal. This is because of fiscal dominance and especially because of a very weak balance sheet that has depended heavily on the Rupee’s slide in order to maintain positive equity. The key policy rate has been kept in negative territory in real terms, which by definition means loose monetary conditions. But more importantly, the lack of a proper balance sheet driven by the lack of willingness to recapitalize the central bank versus letting the rupee slide rebuild its equity base has meant that short term treasuries and the interbank rates have remained well below the key policy rate.

All this, when coupled with a too fragmented local bond market with too many small issues, means that the transmission mechanism of monetary policy to output and prices has remained largely ineffective. In a way, when the car itself is broken, the debate about where rates should be/at what speed one should drive at becomes mute. With the economy showing continued signs of overheating given above potential growth (potential growth in Mauritius is between 3% and 3.5%) and obvious skilled labour shortages, with inflation expectations remaining loosely anchored, with real interest rates remaining negative and with inflation well above the medium term target, it is obvious that interest rates should be higher. But given the sorry state of the central bank balance sheet, fiscal dominance and the soon to be discussed household debt conundrum, this discussion becomes mute. The Rupee’s slide is hence a reflection of the lack of credibility of monetary policy and overall macroeconomic imbalanced versus exogenous trends alone.

The Rupee’s slide is a reflection of the lack of credibility of monetary policy.

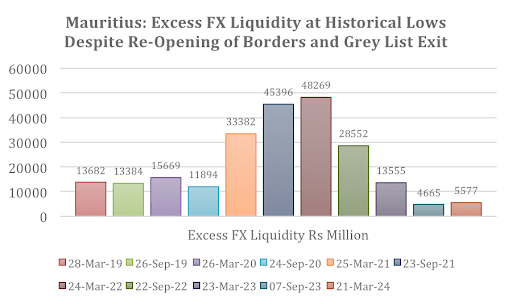

Local bank forex excess liquidity remains well below pre-Covid levels

The impossible trinity in monetary policy means that a country cannot have an independent monetary policy, open capital flows while controlling the level of the exchange rate at the same time. The Bank of Mauritius has finally begun to understand this basic concept, after having borrowed more than USD 1.5 billion in order to bloat the value of international reserves, offset large market losses in its fair value through profit and loss portfolio and to finance unsuccessful interventions.

While the central bank has attempted to control foreign exchange demand via rationing despite the re-opening of borders, fiscal policy, which privileges the debt-fuelled consumption model, has rendered its efforts ineffective given the pressure that this model has on the currency and thereafter on inflation itself. As the chart below showcases, despite the forced imposition of foreign currency rationing, policy makers have been unable to offset rising demand-fuelled imports with higher exports. Negative real interest rates, the lack of monetary policy credibility and the lack of macroeconomic buffers have in turn continued to put pressure on demand as reflected by the low levels of excess foreign exchange liquidity available at local banks.

Unless the government engages in meaningful structural reforms, gradually recapitalizes the central bank (without using depreciation as a tool to do so) and meaningful fiscal consolidation, local buffers will remain weak.

Weak macroeconomic buffers in the era of perma-crises

Total private debt in Mauritius today stands at more than MUR 483 billion, including Global Business Companies which, when summed with public debt and the present value of unfunded liabilities (think pension holes and other state liabilities), leads to a kitty that is easily above a trillion rupees. At the same time, the Bank of Mauritius has mismanaged international reserves to such a degree that it has yet to recuperate from large market losses made two years ago, and given the obvious liquidity risks that comes from holding such a large percentage of international reserves in a Hold to Maturity Book. The International Monetary Fund estimated that the Assessing Reserve Adequacy (ARA) metric, which is a more meaningful metric to measure reserve adequacy versus import coverage, is today below 100%, which is below the lower bound of what the IMF would consider as being adequate.

There was a lot of misplaced hope without any proper risk management on a Chagos compensation which never came. In the era of Perma-Crises, Mauritius lacks meaningful macroeconomic buffers, and with populism in fashion with all political alternatives, it is hard to see how this trend will reverse. With any exogenous shock, macroeconomic policy makers would quickly need to let the Rupee slide to adjust and smooth the shock.

The longer term financial stability risks and monetary policy constraints

Governments come and governments go, but some have a much larger longer-term impact than others. The debt-fuelled consumption model favoured by the current dispensation has seen total private debt rise from MUR 362 billion in 2019 to more than MUR 483 billion and counting today. This number is artificially low because the Mauritius Investment Corporation bought “convertible” bonds which anywhere outside of Mauritius would be a laughing matter given that the bad structuring should be accounted as debt versus “quasi equity”. When a convertible has a conversion option with zero value (in this case given bad and biased structuring), it should be treated as plain vanilla debt. Hence the total debt figure should be at least MUR 30 billion higher.

More worryingly perhaps is that household debt has risen from MUR 102 billion in early 2019 to MUR 162.7 billion today. In stark contrast, the large corporates have benefited from ultra-cheap bailouts with coupon rates below inflation and premium pricing for land acquisitions, rupee depreciation and bloated revenues given depreciation and inflation. The private sector in Mauritius has often been characterized by one that focuses on control versus efficiency. More often than not, return on capital employed has been lower than their respective weighted average cost of capital.

The population is on the synthetic drug of money illusions.

Many were asset rich on paper but very free cash flow poor. Their stock prices were not performing well prior to the onset of the pandemic for it. But the pandemic offered the private sector a golden opportunity to transform. State bailouts, depreciation and inflation of land prices have even allowed Zombie companies to become alive again without any sacrifice by shareholders.

Corporates have seen the real value of their debt decline while rupee earning households have seen their borrowings rise. Rupee depreciation and inflation means more household debt is needed to maintain, let alone grow their consumption and purchases of real estate assets. Such a vicious cycle is guaranteed to lead to rising wealth inequality over time and make populist reactions which will be self-defeating to the private sector and in the end worse.

It should also be noted here that prior to the pandemic, the Bank of Mauritius had largely relaxed macro prudential measures to stimulate credit growth especially for households looking to buy real estate assets. One also has to say that the current dispensation has been factually very giving especially when we think about the wage assistance scheme write-off to the private sector versus acting like a neutral referee here to promote free and fair competition. Macroeconomic policies have in a nutshell facilitated the privatization of gains whilst socializing the losses. Bread crumb helicopter money has been dumped on the uneducated and semi educated despite the consequence such policies have on inflation. The population is on the synthetic drug of money illusions.

From creating macro policies to help large landowners bloat asset values to weakening the Rupee and to bailouts and wage assistance scheme liability cancellations, macroeconomic policy making has moved very much to the far right in Mauritius. The speed of the increase in household debt, when coupled with negative real interest rates, the opening up of the land bank to more and more foreigners pushing prices higher and the continued relaxation of macro prudential measures, has led to quite the conundrum for monetary policy in the medium to long term. Even if the central bank balance sheet is fixed, which will take a lot of government debt to do and a lot of time, the result of years of macroeconomic imbalances will mean lower-for-longer interest rates, constrained monetary policy given financial stability risks, and will largely depend on major structural reforms and fiscal consolidation.

Taxation as a tool to incentivize market behaviours

It is imperative that Mauritius rebuilds its macroeconomic buffers by engaging in fiscal reforms which would include wasteful spending cuts and new revenue enhancing measures. Temporary taxes such as rupee depreciation driven windfall profit taxes on local corporates, longer term structural tax reforms such as the imposition of land value taxation which will boost investment and tax rent seekers and speculators and better targeting will go a long way to rebuilding fiscal buffers. Today fiscal policy in Mauritius depends largely on inflation and taxing the consumer given the debt-fuelled consumption model. This model has to change. Corporate taxes similar to the likes of Estonia should distinguish between distributable and non-distributable profits. Policy makers have lost any ability today to use taxation as a tool to incentivize and disincentivize market behaviours because of state capture.

There are a plethora of reforms the government must engage in, one of which would be to start to disinvest from this fascination of government-running public owned companies (for the purposes of patronage politics) which they have run so poorly anyway. Reforming the governance frameworks of state-owned companies, making them more independent, putting the right people at the right places and then listing them post reform to maximize value would go a long way towards enhancing long term productivity in this country.

There is a big need to have meaningful dialogue on the often-taboo subject of having a new deal with the private sector wherein the government would over time encourage free and fair competition, reform the competition commission and encourage foreign direct investment beyond real estate. Oligopolies should be ready to compete especially when the bulk of their future investment plans lie abroad.

Real free market capitalism, not state capture

On the monetary policy front, it is important that the central bank’s balance sheet woes become less dependent on a weaker Rupee, which would require public debt funded recapitalization (hence the need to tax) and greater central bank independence. The cost of recapitalization, which should be based on proper estimates of capital requirements based on tail risk measures, would run in the tens of billions and would need to be done over time given the high cost. While many keep on talking about another body taking over the Mauritius Investment Corporation, the reality is that this would require the government borrowing more money to fund the purchase of MUR 55 billion. It is also very clear that the valuations the MIC has done is artificially high given bad structuring. There is no scope for any public entity to even pay for MIC assets at 30-40% discounts.

Macroeconomic policy making has moved very much to the far right in Mauritius.

In any event, this balance sheet hole on the Bank of Mauritius’ balance sheet would be counterproductive at this stage. Taxation and levies on banks that benefited from such badly structured one-sided convertible bond deals would merely correct past mistakes and should be done. The private sector must be one that does not suffer from moral hazard and rent seeking syndrome. It must be competitive, efficient and carry the economy forward. We need real free market capitalism, not state capture in Mauritius.

The Mauritian Rupee at the end of the day, despite short term manipulations and rationing, is a real reflection of the country’s relative stagnation in foreign currency terms. It will not be fixed without fixing the macro-economic imbalances, and this will initially be painful and face significant resistance from those that have benefited from it. Whether the drugged up on fiat currency money printing voter is willing to understand this and demand such changes is of course another matter.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Stay In Touch