By Sameer Sharma

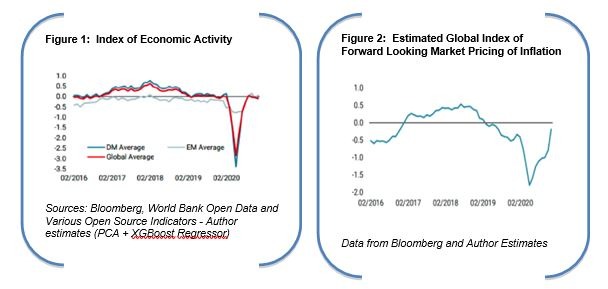

As we look forward to 2021 and to the prospect of vaccines allowing us to get our lives back in order, from an economic standpoint at least, the world economy has recovered well and the COVID impact is looking shallower than what was initially thought. When applying non-linear machine learning ensemble models to a combination of both higher frequency economic data and alternative economic data across regions as showcased in Figure 1, global economic activity has largely recovered mainly led by East Asia and the United States. While a mild dip is likely during the first quarter of 2021 given the partial curfews and partial lock-downs in some regions, global economic growth is on pace to exceed 5% next year and has already mostly recovered to previous levels of economic activity.

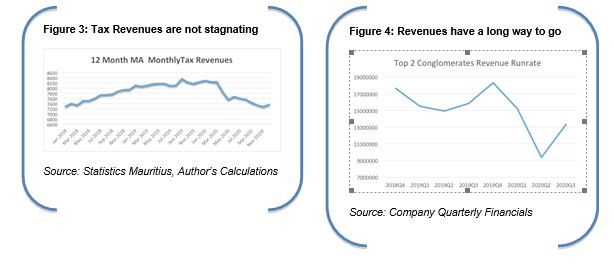

As global economic slack slowly begins to recede in the context of ultra loose monetary policies and given the recovery, global inflation indicators have begun to rise. A simple de-noising of various forward-looking market pricing of inflation in the United States and in Europe indicates that inflation risks are once again rising. While global inflation is likely to be at least 1% to 1.5% higher over the coming five years when compared to the previous 5-year average, shorter term inflation risks should not be dismissed especially as we head closer to 2022.

The post COVID world (if the vaccines work as advertised and are distributed efficiently) will be one where previous secular trends such as digitalization (e-commerce, Artificial Intelligence, robots), inequality, de-globalization, US-China tensions and a focus on economic sustainability (think ESG) will accelerate. This will be a tougher world where offshore tax jurisdictions will increasingly be targeted by the usual tax authorities and where those who compete and innovate will succeed while the rest will not find it as easy as before. When we think about Mauritius, the solutions for the necessary transformational structural reforms are many and overdue, but the political willingness to engage in such reforms is sadly lacking because of what this could do to the system that got politicians elected in the first place.

The system of patronage will not take this economy to the next level

Before Mauritius can engage in meaningful structural reforms, it must decentralise economic policy making away from the office of the Prime Minister, and it must revive technocracy and chose meritocracy over loyalty and idol worship of the Prime Minister. To be fair, the system has always been this way because the political system was designed that way at varying degrees, but this system of nominating loyalists irrespective of competence (and more often than not irrespective of relevant experience in the field prior to the nomination) who are then more than happy to worship and allow their institutions to be remote controlled from elsewhere has not and will not work any more.

Slogans that Mauritius was a “high-income economy” may work with too many on the island, but whether you look at the quality of human capital, the lack of productivity and innovation, the depth of the capital markets, the dependence on financial flows and tourist receipts which helped keep skeletons under the carpet, rising debt, subdued private investment especially when excluding bricks and mortar related investments, an increasingly unsustainable tax system given the rising cost of the welfare state, demographic trends and stagnating pre-COVID economic growth, the true picture is much more complicated.

You need smart people who can take decisions rather than waiting on orders from elsewhere.

Sure, the system of patronage may win elections but it will not take this economy to the next level. You need independent and competent technocrats in key institutions of this country who act independently but are accountable. You need smart people who can take decisions rather than waiting on orders from elsewhere. Mauritians of course also get the system and the politicians they deserve. Politicians love to be worshipped as demigods on the tiny island nation, but too many like to engage in the worshipping too.

In a country where alternative job opportunities are few and living costs are ever rising, many will play the “dance to the tune of the powers of the day” game and pick up the nominations even if they are not qualified for the post. Many of us who have attended parties where recently elected politicians suddenly get invited and become the canter of attention will laugh about it to some others, but all of this tamasa is why Mauritius will struggle in the years to come. The notion that a potential nominee would say “thank you but I have to refuse because this is not my field and I am not qualified for this role” does not really exist in Mauritius.

Over the past 40 years, all of us who live or have lived and worked in Mauritius have been tempted to go on the “if we cannot beat them, let us join them” route and too many have done so. Those who do not play such games typically stagnate or leave the country. Mauritius is a small country with a small reservoir of competent technocrats, and the more it closes the inner circle of those who make decisions, the worse it will be and has been.

The rising number of Zombie companies post-COVID will have longer term implications on private sector investments, job creation and potential output.

A lot can be said about some in the private sector too of course. This notion that we need diversified Jack of all trades but Master in none businesses despite poor free cash flow levels and ROCE (Return on Capital Employed) versus WACC (Weighted Average Cost of Capital) metrics, the over-reliance on debt rather than on optimal debt and equity funding mix (long periods of excess liquidity in the system distort credit risk pricing and behaviour), a passive shareholder base, the lack of competitiveness, insular thinking by some captains, “quand la construction va, tout va” approach and a saturated and small market are all factors which explain why the government has had to step in with massive debt and grant funded public investments which have not always had strong multiplier effects on the economy pre-COVID. Right now the Bank of Mauritius has provided regulatory forbearance which has pushed the credit risk can down the road a bit further, but the rising number of Zombie companies post-COVID will have longer term implications on private sector investments, job creation and potential output. You can play with rules and make things look better than they are on paper, but reality bites on all the same.

The benefit of printing money is fast eroding

Whatever I have said so far can be seen in the data too. Mauritius is already lagging. The Bank of Mauritius is printing large sums of money, but the pre-COVID structural ills, the black listing and the closed borders means that all this printing is having little effect so far. I supported and pushed for unconventional monetary policies way back in February 2020 and still do but mainly when it is driven towards the credit channel (not like what is being done with the Mauritius Investment Corporation of course – a good idea gone bad by not having the right people at the right places as usual) and more importantly when it is associated with clear policy guardrails.

Very few in Mauritius understand how complicated it will be for the central bank to efficiently manage its balance sheet and be a credible inflation fighter in the coming years. The asset liability management of its balance sheet in any rising inflation scenario would require an amendment to the Bank of Mauritius Act in order to allow the central bank to go into negative equity territory so that it can credibly focus on fighting inflation. Those who think otherwise have simply not done the math.

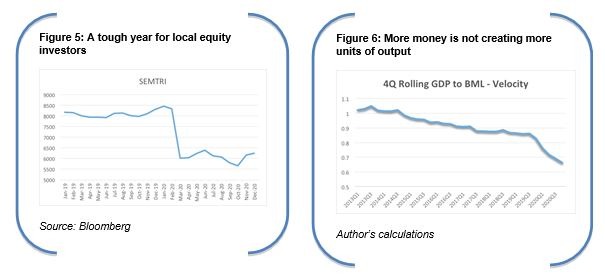

Mauritius, unlike the rest of the world as can be seen in Figure 3, is still struggling. Tax revenues give us a good sense of what is happening to corporates and to the consumers, and this metric is quite correlated to local growth. It is not rising!

The two largest conglomerates, namely IBL and CIEL, are diversified across multiple sectors of the economy, and their quarterly revenue trends also offer us some insights about the pace of any economic recovery as showcased in Figure 4 (note that GDP numbers in Mauritius lag and are still stuck at second quarter of 2020 – you can all guess why it takes us longer than the rest).

With tourism earnings not expected to recover in December 2020 and with a weakened Mauritian consumer (as showcased by tax revenues), one should not expect any meaningful recovery in those topline numbers soon. More generally, the Mauritian stock market is in the last decile of the worst performing stock markets in the world in 2020. The graph of the local market (Figure 5) reflects the state of challenged corporate balance sheets and revenue declines and seems to be one more higher frequency indicator which points to the still MIA recovery. The stock market is certainly an imperfect indicator but it is well aligned to other indicators too (in a country where sadly high frequency data is still not plentiful in 2020 given the politics around it).

From Figure 6, we can see that the velocity of money (the same trend is observed if you use base money versus M3) decline has accelerated in recent quarters. We can print but it is not generating a lot of growth because of our structural ills pre-COVID, the blacklist and the closed borders. The only positive from this picture is that given low global inflation over the past decade (imported inflation pressure was low), high growth in both base money and M3 did not lead to higher domestic sourced inflationary pressures since the economy tended to operate below capacity/potential. The significant slack still found in the Mauritian economy today means that shorter term domestic sources of inflationary pressure are unlikely to play the spoil sport despite all the money printing, but if we start getting more inflation from abroad or even if we begin to get a more meaningful recovery after the opening of borders in the coming 2 to 3 years, then the chart below will put the Bank of Mauritius in quite the conundrum.

A country can print all the money it wants for a time but if it cannot increase its capacity to produce more goods and services with it, then it will turn against the country. How long can Mauritius keep on printing money, pretend that it has near zero fiscal deficits given monetization and not see growth pick up? It has been six months since Mauritius emerged from a successful lock-down, and Figure 1 has shown that the world is already moving on, but it does not yet seem clear to this author at least that policy makers have engaged in meaningful introspection about why their policies are not working as the benefit of printing money is fast eroding.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Stay In Touch